GameWhat?Who is good? Who is evil? Who is right? Who is wrong? Let me share what I found interesting throughout all this, maybe clear up some misconceptions, and maybe you’ll leave this letter more informed, conflicted, or entertained. So let’s talk about the events of the last week or so of this $GME (GameStop) saga. Here’s some of the TL;DR breakdown of some of that things that have caused many “interesting” things to happen as of late. TL:DR -

It’s imporant to understand what a short squeeze is, so here’s a high-level explanation. What is a short squeeze?In a short, people borrow shares to bet against a company. They eventually need to buy those shares back to cover their negative position. If the folks that actually hold the shares, or in this case $GME, decide that they don’t actually want to sell their $GME back to the short sellers, the price can run upwards out of control. When you buy, the price rises = added demand. When you sell, the price falls = added supply. When there are too many shorts, the price can rise rapidly because everyone is buying back at market price (closing their position) to avoid their shorts going underwater. This is called a "short squeeze" also known as a “gamma squeeze.” Why was there a short squeeze?Are traders from the subreddit WSB (WallStreetBets) really that smart? No…And yes. The story of GameStop didn’t begin with a movement or some grand scheme to dumpster Wall Steet and take on hedgefunds. It had more humble beginnings. Think of a cocktail composed of deep fundemental analysis/research (as deep as any hedgefunds) and degenerate yolo gambling, usually with spare cash, and sometimes with life-savings (fundementally, no different than a hedgefund or some other institutional player, ‘cept the bailouts). If you were to dig into some of the earlier posts on WSB about $GME, you’d find plenty of folks discussing P/E value’s (price to earnings ratios), partnerships, events, listening in on earnings calls, etc…all things that we would consider “fundemental analysis,” that is, a way to determine a stocks fair market value.

In yesterdays interview with CNBC’s Scott Wapner and Chamath Palihapitiya, Scott kept asking Chamath “where is the fundemental analysis” (to justify a $350 share price for GameSpot)

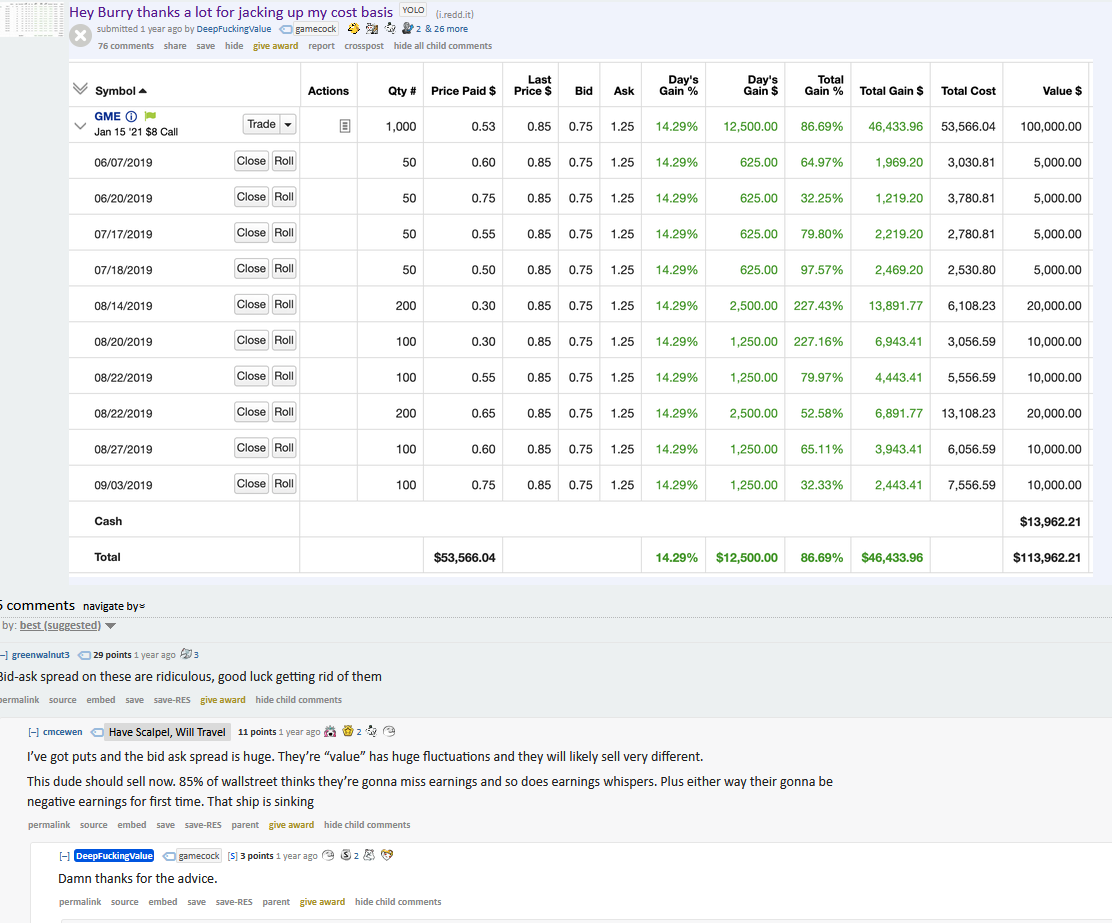

Well, it was there. It exists. Believe it or not, there were folks on WSB who were doing decent fundemental analysis on GameStop. But there was also meme magic at play. Did you notice the title of that post by WSB’s DFV (DeepFuckingValue).

Burry is a reference to Michael Burry, who was meme’d into Wall Street lore with the 2015 film The Big Short (about the build-up/crash of the United States housing bubble during the 2000s).

Well, as it turns out, the real Michael Burry (see below) has been long on $GME since atleast August 2019.

His thesis? Discs.

Discs? Yeah, discs. He believed that both console makers (Sony and Microsoft) would be putting disc drives in their respective next-generation game consoles. If you’re not in my generation, and have never been to a GameStop, and have never tried to sell something to a GameStop, you might not understand why this could be a bullish catalyst for GameStop. Basically, customers bring in their game discs, which GameStop purchases in store credit or cash. Those game discs are then re-sold at a markup. Boom profit.

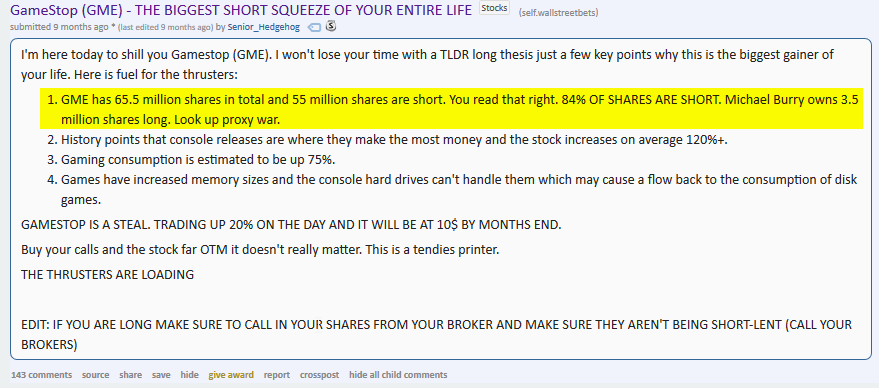

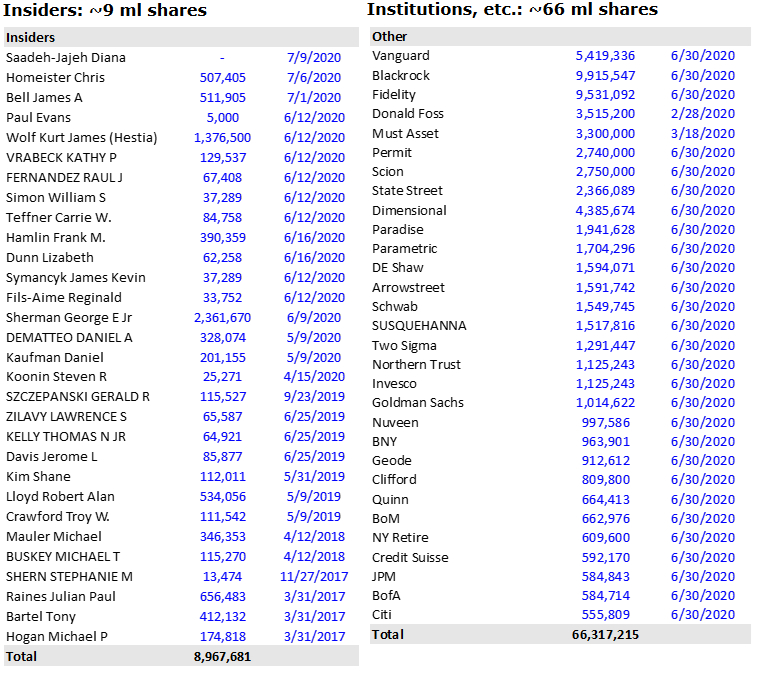

So Michael Burry’s fund (Scion Capital) bought a small stake in GameSpot, and by small I mean ~3,000,000 shares, or 3.3%, of GameStop Corp. common stock (the initial investment was worth ~$10.6 million). Back to Scott Wapner from CNBC and his “where is the fundemental analysis?” When you combine meme magic, character Michael Burry, WSB, the potential to make money, some trolling, being part of a community, and just having a good time, fantastic things can happen. Let’s take a look at some of of the analysis that was being shared/discussed on WSB, specifically towards a case for a short squeeze. The Short Squeeze Case StudyWhat I’m trying to point out in the screenshot below (from April 14, 2020) is that folks who were discussing $GME were keenly aware of $GME’s outstanding shares, what short-lending is, and are hardly the dumb retail investors news media has been portraying them as. They’re just intelligent gamblers.

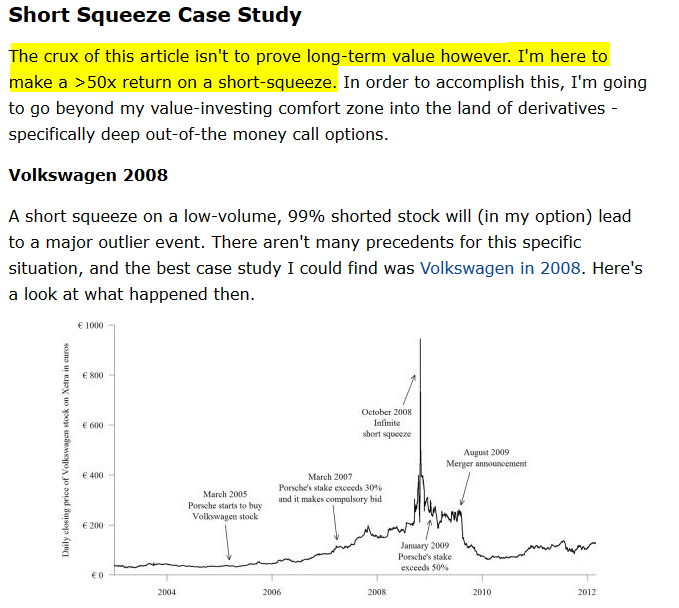

This section will be a reference to a SeekingAlpha article by Jonathan Prather I included the screenshot below for those of you who are still like “But Muh ValuE”. This wasn’t a trade on the fundemental value of GameStop.

Jonathan continued this case study by discussing GameStop ownership,

Check out our boy Micheal Burry (Scion) who was still holding 2,750,000 shares as of 6/30/2020.

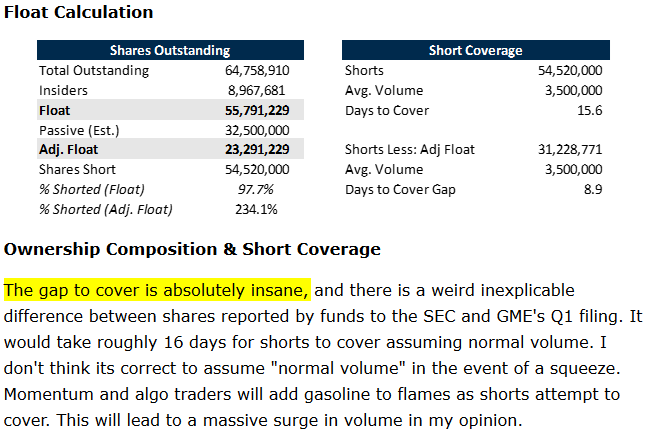

Jonathan also did a great job with his float calculations.

Jonathan goes on to review console sales figures, industry margins, and option pricing models (which 99.99% of the population will never understand, and this is not an exaggeration).

How can there be more shares than actually exist?Jonathan brough up an interesting point in his analysis, that is “how are there more more shares of $GME than actually exist?” This was because GameStop was massively over sold. How oversold? 136% of GameStop was short. 36% more shares of GameStop were being shorted, then actually exist. How is this possible? RehypothecationImagine you get a mortgage and buy a house. What’s actually going on is that you pledge to give up the house unless you can pay back the loan back. The bank "hypothetically" owns the house, even though you get to keep it. When you secure a mortgage, you technically own your home. But it is also collateral for that loan. Which means lenders can reposses it if you default on payments. This is the process of hypothecation. Now, what can happen is that the bank can then take that house and borrow against it, just like you did. The people your bank borrows from "hypothetically" own your house, even though you get to keep it. This is the process of rehypothecation. Althought the Federal Reserve has research that says suggest rehypothecation is mostly okay, you do create a daisy chain of liabilities. And the longer the chain, the more likely a failure at any point in the chain leads to an inability to pay back debts all across the chain. “Rehypothecation was a common practice until 2007, but hedge funds became much more wary about it in the wake of the Lehman Brothers collapse and subsequent credit crunch in 2008-09.” (Investopedia) Tl;dr - It’s an asset used as collateral more than once, at the same time. Back to GameStop stock being 136% shortImagine company COINSHEET has 1,000 outstanding shares. And 800 of those shares are with institutions that participate in stock lending programs. Short sellers borrow those 800 shares, and sell them. Suppose now 600 of those 800 shares end up with institutions that have stock lending programs. Short sellers can now borrow those 600 shares and sell them again. And again. And again. (This part of one of those screenshots above from WSB’s should make more sense now.)

To quote Chamath from his Jan 27 interview on CNBC -

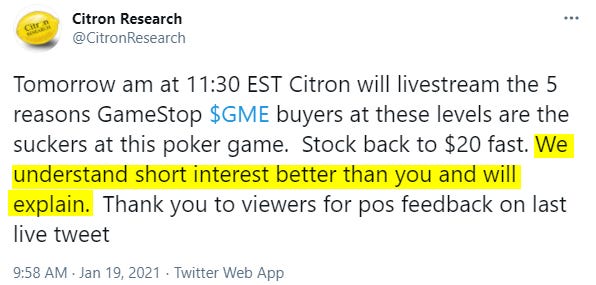

$GME was over-shorted at 136%. People found out, talked about it, and said that demand would outpace supply if they bought everything up and held. That’s basically it. Citron, Robinhood, Citidal, Melvin Capital, etc…As a general rule of thumb, it’s usally not a good idea to call a large group of people dumb, especially when they have skin in the game. How it started:

How it’s going:

It is somewhat hilarious that shorters are getting all this media flak when shorters at places like Muddy Waters Research were the ones who were on RETAIL’s side when they exposed scams and frauds (during the early 2010’s shitcoin era of Chinese direct listing in the NASDAQ). They exposed scams & frauds and the shorts were them showing their conviction, by putting money where their mouth is. Anyways, super interesting stuff, if you’re interested check out the move The China Hustle.

And now the people are meming them into pain. (It’s funny thought, and they can probably take it, so no worries). Robinhood front running tradesThis was popular on Twitter, and kinda innacurate so I wanted to address it.

Front-running stocks is illegal everywhere. When Robinhood sends your orders to Citadel (and other market makers who pay for the order flow) market makers don’t front-run your orders — they’re required by Regulation NMS to execute your order at the best price among all of the exchanges (even thought this doesn’t always happen and get they fined millions for it). The reason why they want the orderflow is because they think you’re a baddie and they want to get first priority to trade against you. If you’re interested in how discount brokerages make money, I can recommend this article. Here’s an excerpt:

In conclusionThere still isn’t a conclution. We’re all sitting on the sideslines watching the world unfond. Meme’s are slapping. Google is doing Google things.

Billionaires are losing money, and billionaries are making money. WSB’s discord server gets taken down, Robinhood halts trading of GameStop and a bunch of other WSB favorites. Lawsuits, tales of insider information, inner circle manipulation, etc… DVF is still holding over $33mm (down $14.8m from $48mm the day prior) in $GME on his initial $50k investment.

And what’s looming on the horizon is a bubble, a bubble that will inevitably pop. But unlike most other bubbles, the story of this one is ours. The endSee you later space Cowboy © 2021 CoinSheet LLC Unsubscribe

|